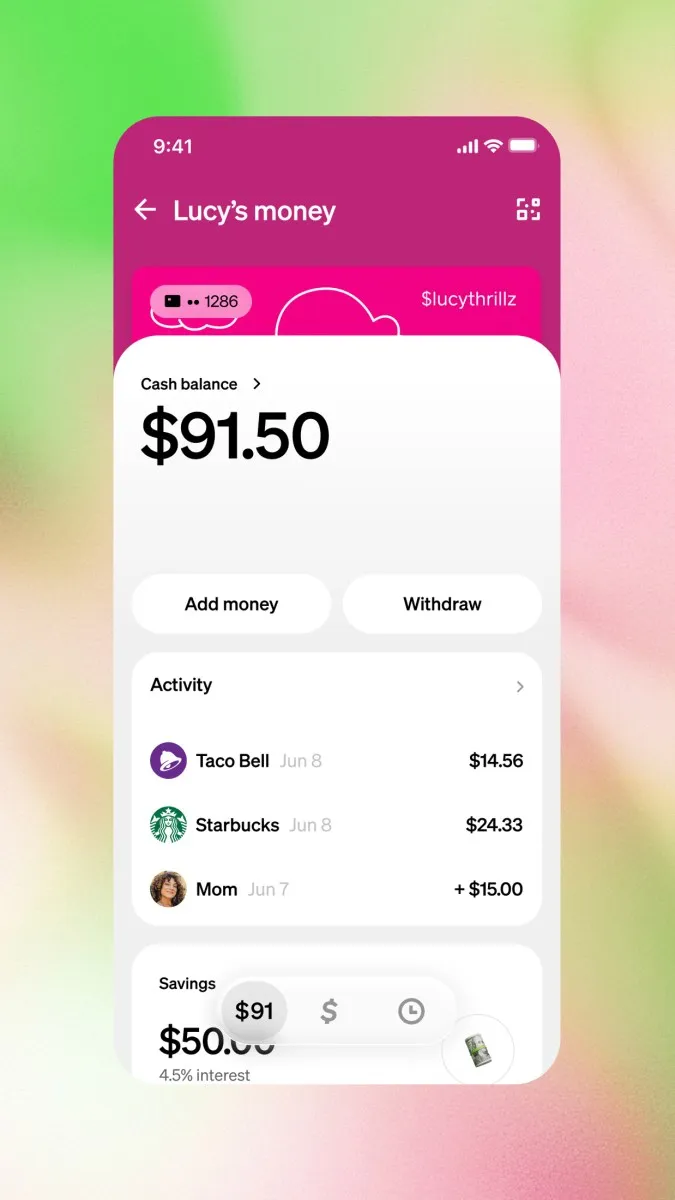

Cash App, the fintech platform owned by Block (formerly Square) and founded by Jack Dorsey, is expanding its financial services to a new and notably younger demographic: children aged 6 to 12. This strategic move marks a significant evolution in the company’s youth-focused offerings, building upon its existing suite of teen accounts to now include pre-adolescent children in a parent-managed financial ecosystem. The initiative, announced this week, allows parents to create and manage financial accounts for their children within the Cash App ecosystem, though the children themselves will not have direct access to the app interface. Instead, parents retain full control over deposits, monitoring, and transaction approvals, while children receive a physical debit card linked to the account that they can use to spend allocated funds.

The accounts are designed not merely as spending tools but as educational instruments aimed at fostering early financial literacy. According to Kristen Anderson, group product lead for Core Networks at Cash App, the program is intended to teach children about savings, budgeting, and financial responsibility through interactive features such as savings goals and the platform’s existing "allowance" functionality. This feature enables parents to schedule automated, recurring transfers to their child’s account, simulating a regular income stream and encouraging disciplined money management habits from a young age.

In addition to parental funding, the accounts can receive peer-to-peer (P2P) payments from a limited set of pre-approved users — such as grandparents or other trusted family members — further integrating the child into a safe, supervised financial network. Notably, Cash App claims these youth accounts will be eligible to earn up to 3.25% in annual interest on balances, a feature uncommon in traditional children’s savings products and indicative of the company’s effort to make saving tangible and rewarding for young users.

The program also includes a clear developmental pathway: upon turning 13, and with parental consent, children can "graduate" to their own independent Cash App accounts. At this stage, they gain access to a broader range of services, including the ability to buy and sell Bitcoin and trade stocks — though these activities remain under the supervision of a "sponsored account" model, requiring ongoing adult approval and monitoring until the user reaches the age of 18.

Cash App already reports having approximately 5 million monthly active teen users, according to Owen Jennings, executive officer and head of business at Block. This established user base provides both validation and infrastructure for the expansion into younger age groups. The company’s move comes amid a growing trend in the fintech sector, where platforms are increasingly targeting minors with financial products aimed at promoting financial literacy. Examples include Step, which recently attracted regulatory scrutiny following its acquisition by MrBeast (Jimmy Donaldson), the popular YouTuber and TikTok personality, raising concerns about influencer-driven financial products and their potential impact on young, impressionable users.

Proponents of youth financial tools argue that early exposure to banking concepts, saving, and responsible spending can lay a strong foundation for lifelong financial health. They emphasize that in an increasingly cashless society, familiarizing children with digital money management is not only practical but necessary. Critics, however, caution that such platforms may inadvertently normalize consumerism, expose children to financial risks too early, or blur the lines between education and commercial engagement — particularly when tied to high-profile influencers or gamified spending experiences.

Despite these debates, Cash App’s latest initiative reflects a broader industry shift toward embedding financial services into the formative years of childhood. By combining parental oversight, tangible tools like debit cards, interest-bearing accounts, and educational features, the company aims to position itself not just as a payment processor, but as a long-term financial partner beginning in early childhood. As Gen Alpha — the cohort born roughly between 2010 and 2025 — comes of age in a world dominated by digital transactions, platforms like Cash App are betting that early engagement will translate into lasting brand loyalty and financial engagement.

The announcement was covered by Lucas Ropiek, a senior writer at TechCrunch who specializes in artificial intelligence, consumer technology, and startups. He previously reported on AI and cybersecurity for Gizmodo and can be contacted via email at lucas.ropek@techcrunch.com.

Cash App Targets Children Aged 6–12 with New Youth Financial Accounts